Very interesting insights were shared by Nilesh Shah from Kotak Mutual Fund via the Monthly Update. I am sharing some nuggets out of the overall insights are in this thread. This blog note is an extract from our twitter handle @banyanfa with some additional commentary from my end. Please follow it for regular updates.

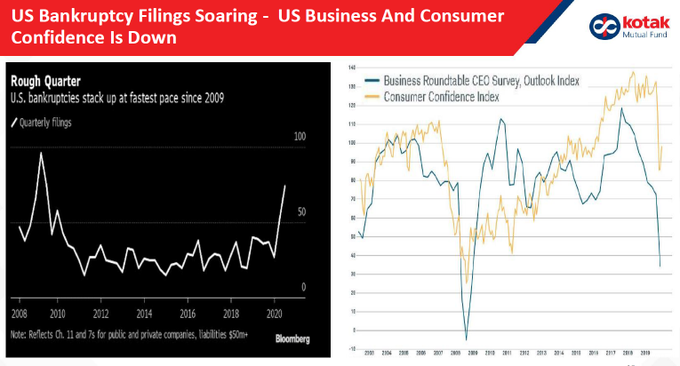

Grim scenario with increasing US bankcrupcies and dropping confidence Indices.

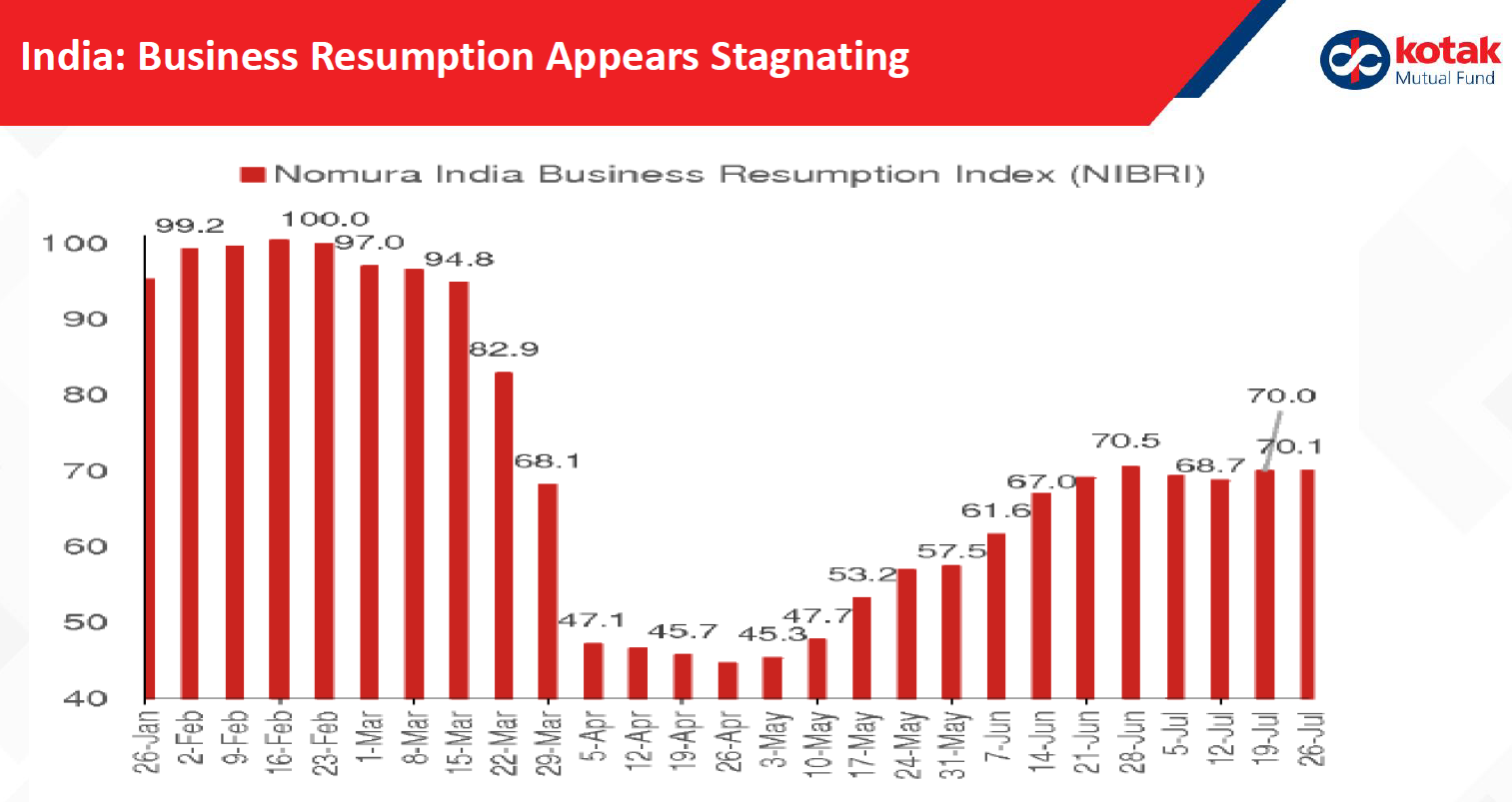

Post the lockdown, the Business resumption index from Nomura went up from 45 levels to 70 in June. However, post that, it has been stagnant at these levels, yet far from 100 post lockdown levels.

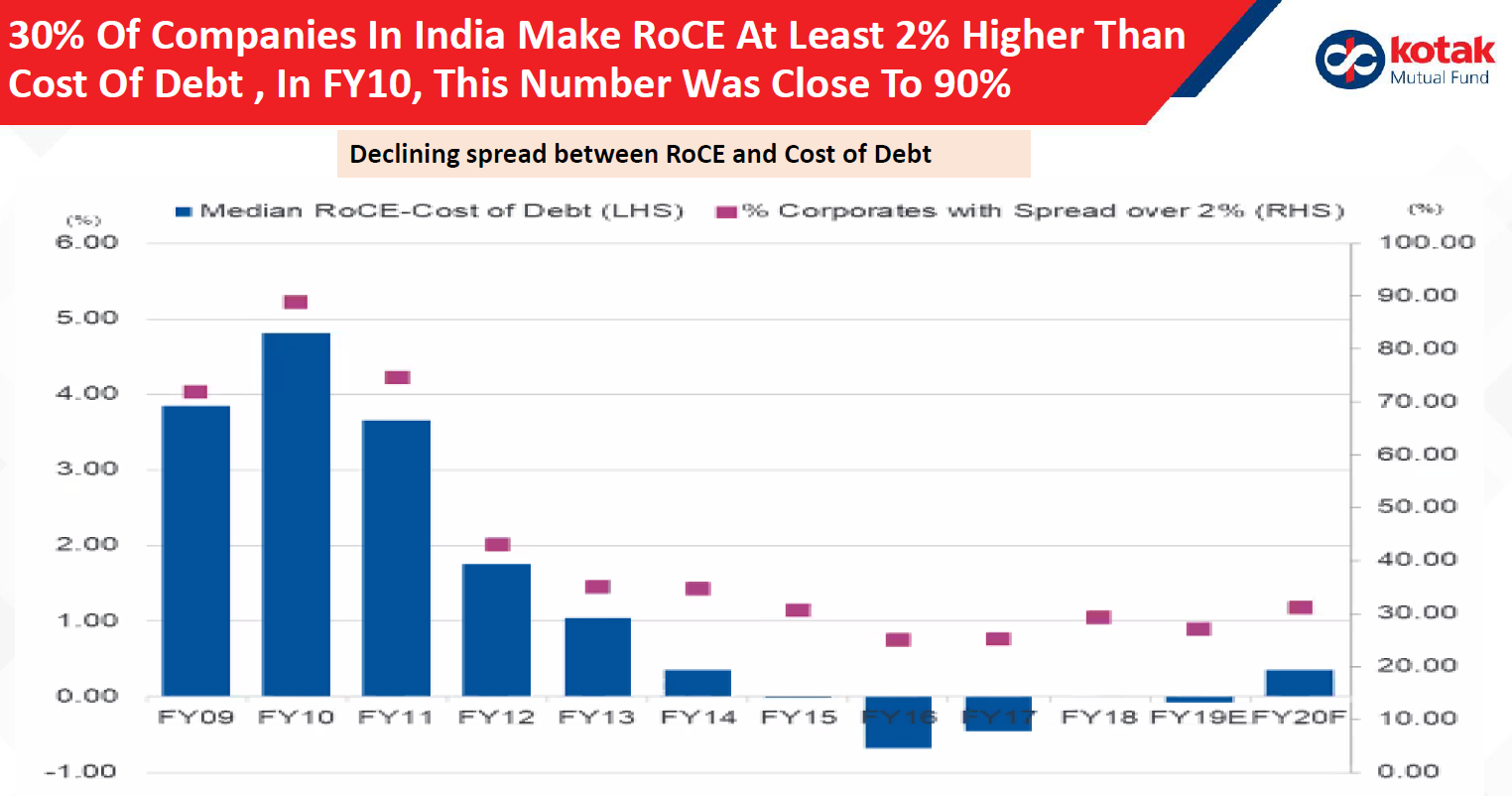

Return on Capital Employed has declined steadily since 2010. In 2010, 90% of the Companies earned ROCE higher than the rate of loan. Now this is 30% of the Companies.

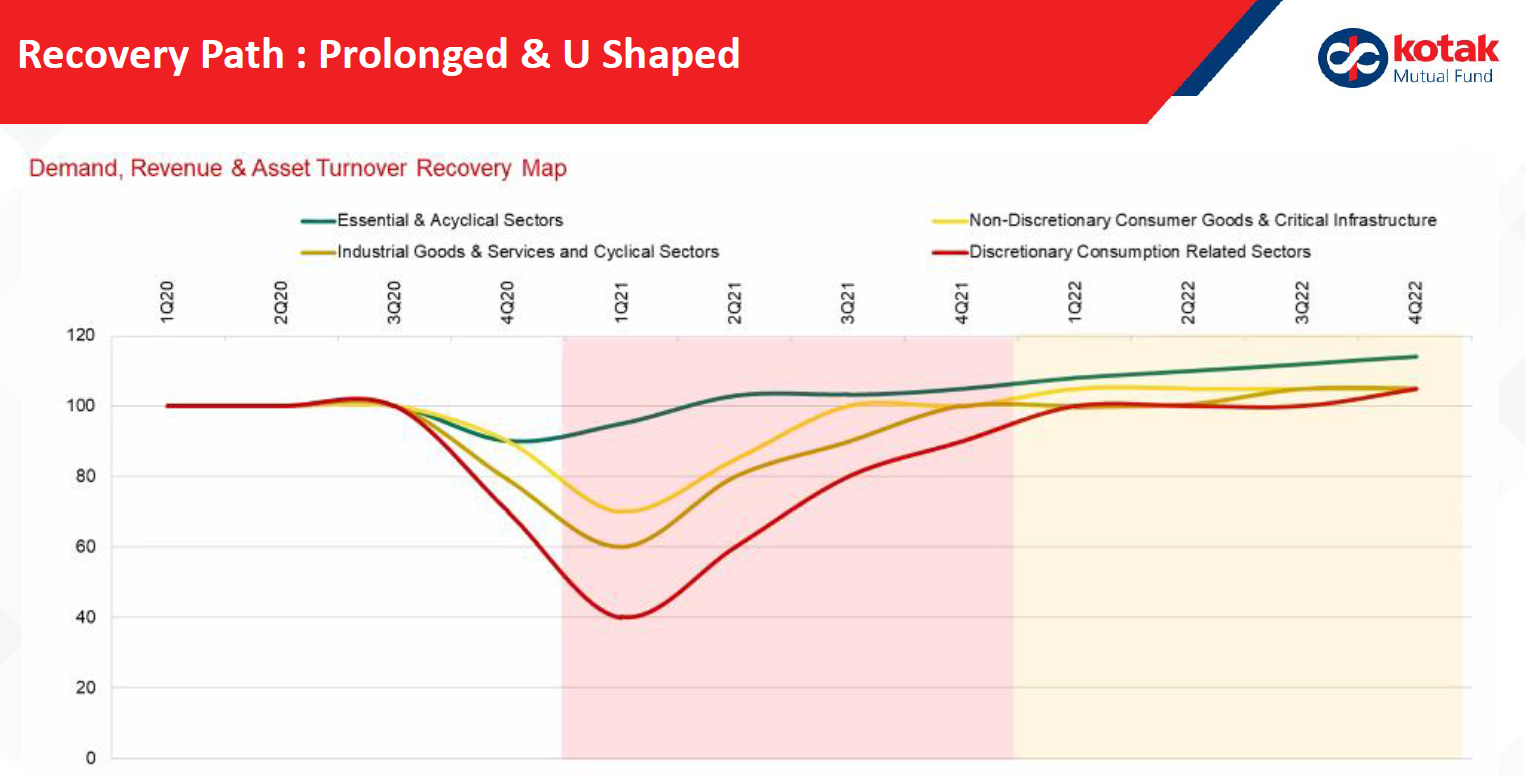

Depending upon the type of business, the recovery will be smooth to painful. For example, the Discretionary Consumer spending, e.g. Travel & tourism, it will have a significant decline and the longest recover. However, for Essential items, the impact would be minimal (green line)

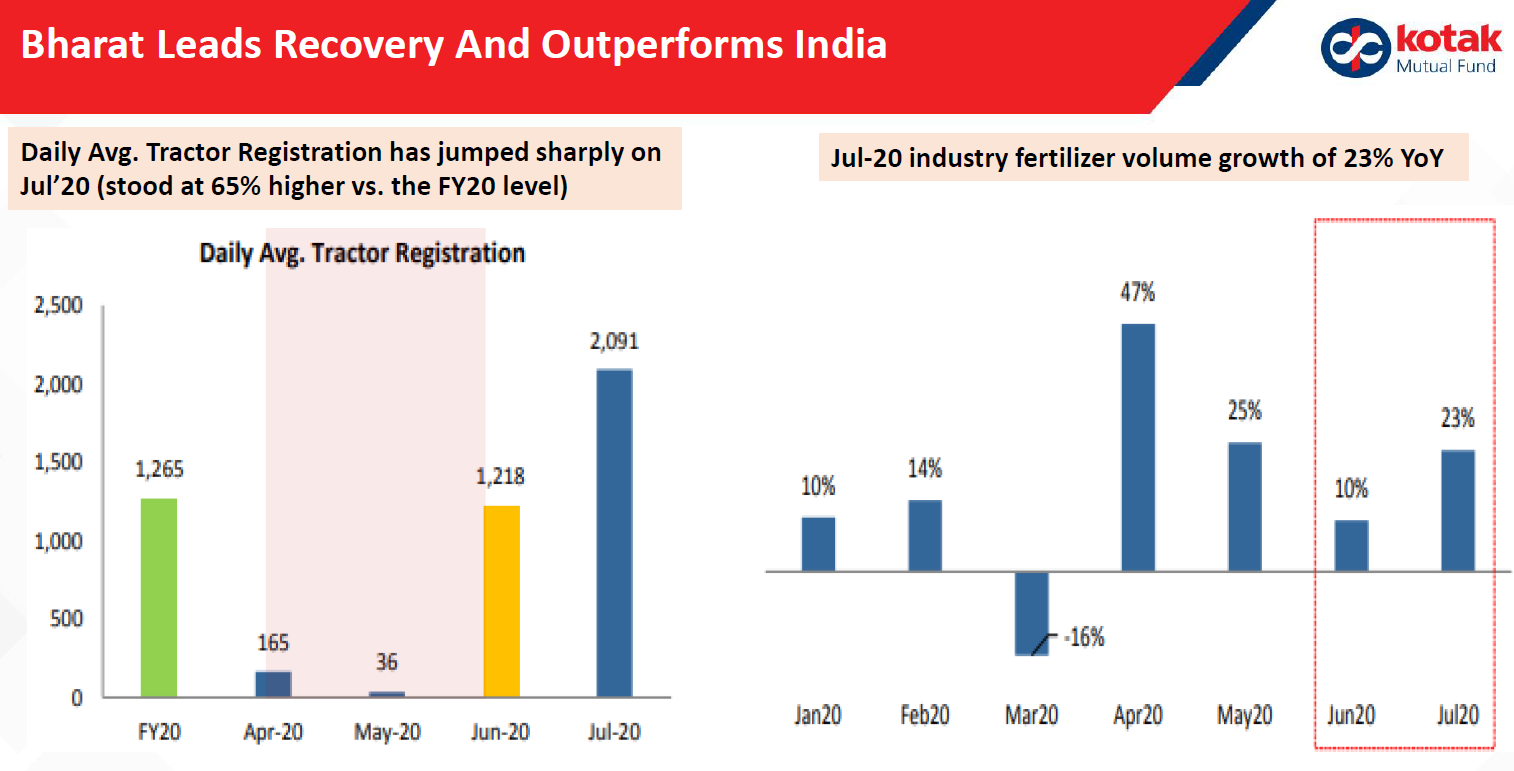

Recovery is being led from Rural ‘Bharat’ rather than wider Urban locations. This is witnessed via Tractors and Fertilisers growth

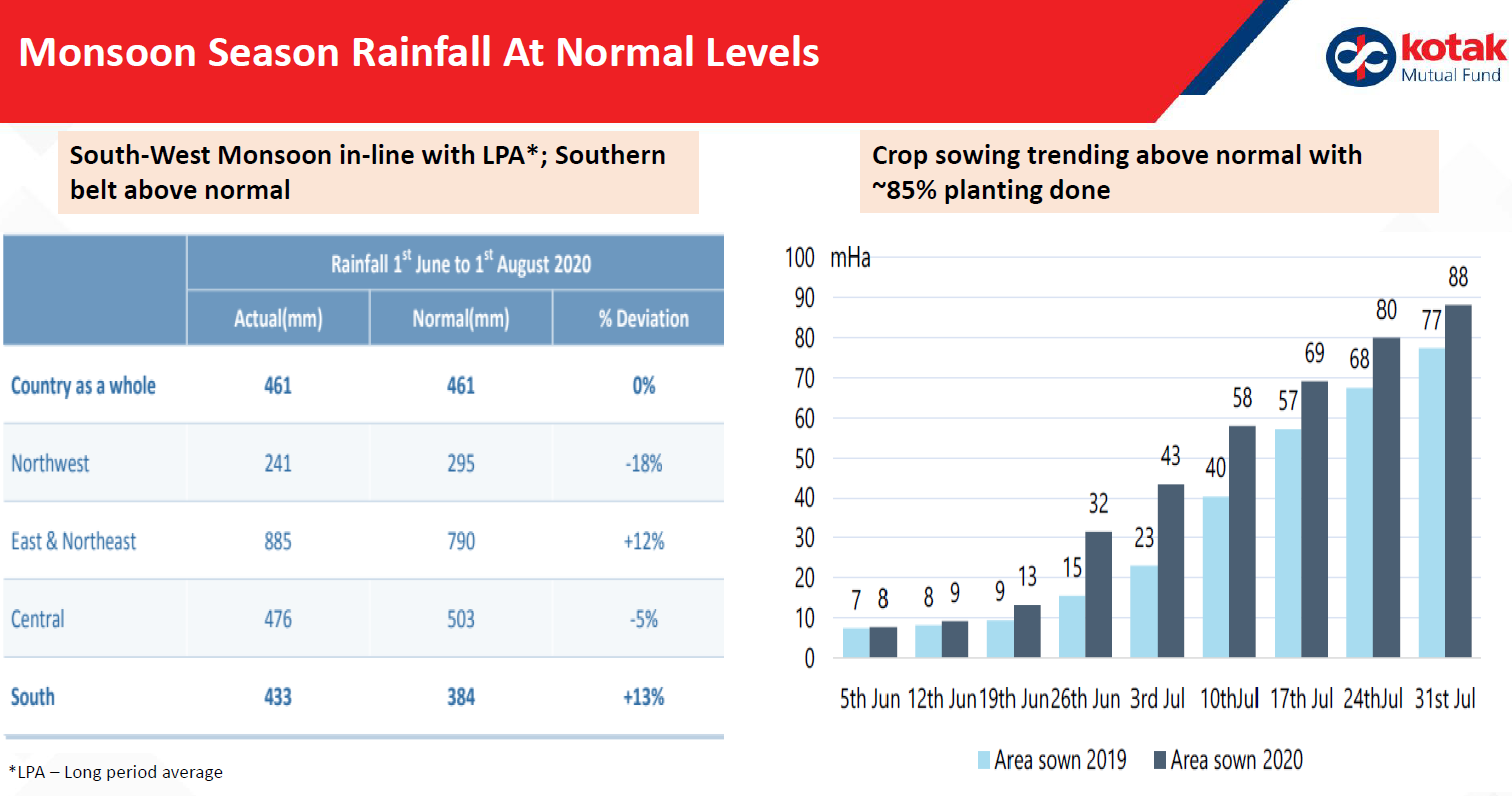

Monsoon is of great support with current rainfall nicely spread across the country and at long term average. This aids sowing activity.

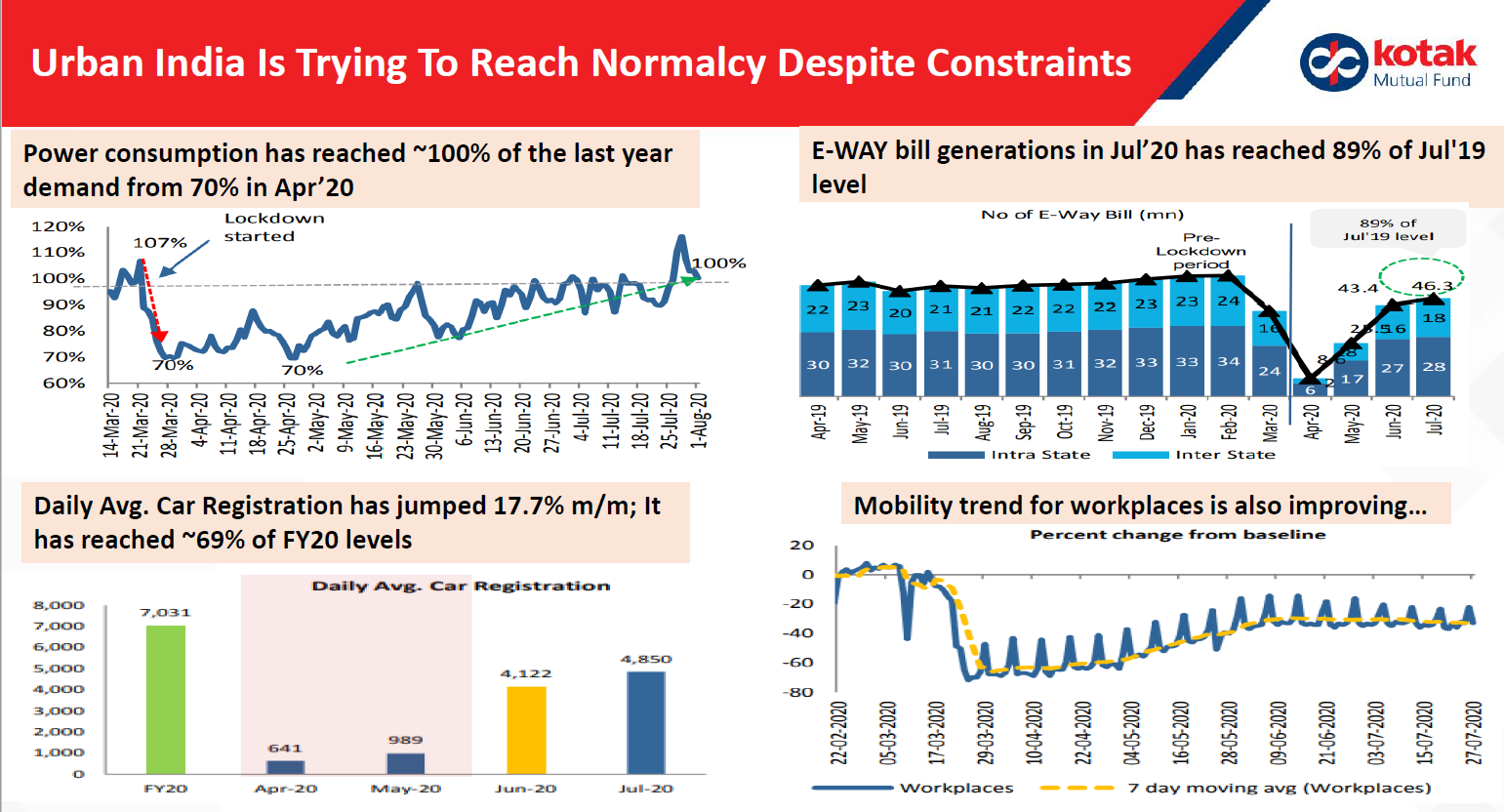

Gradual recovery is also being witnessed in Urban cities via data points such as Power consumptions, car registrations, GST eWay Bill generations indicating movement of goods

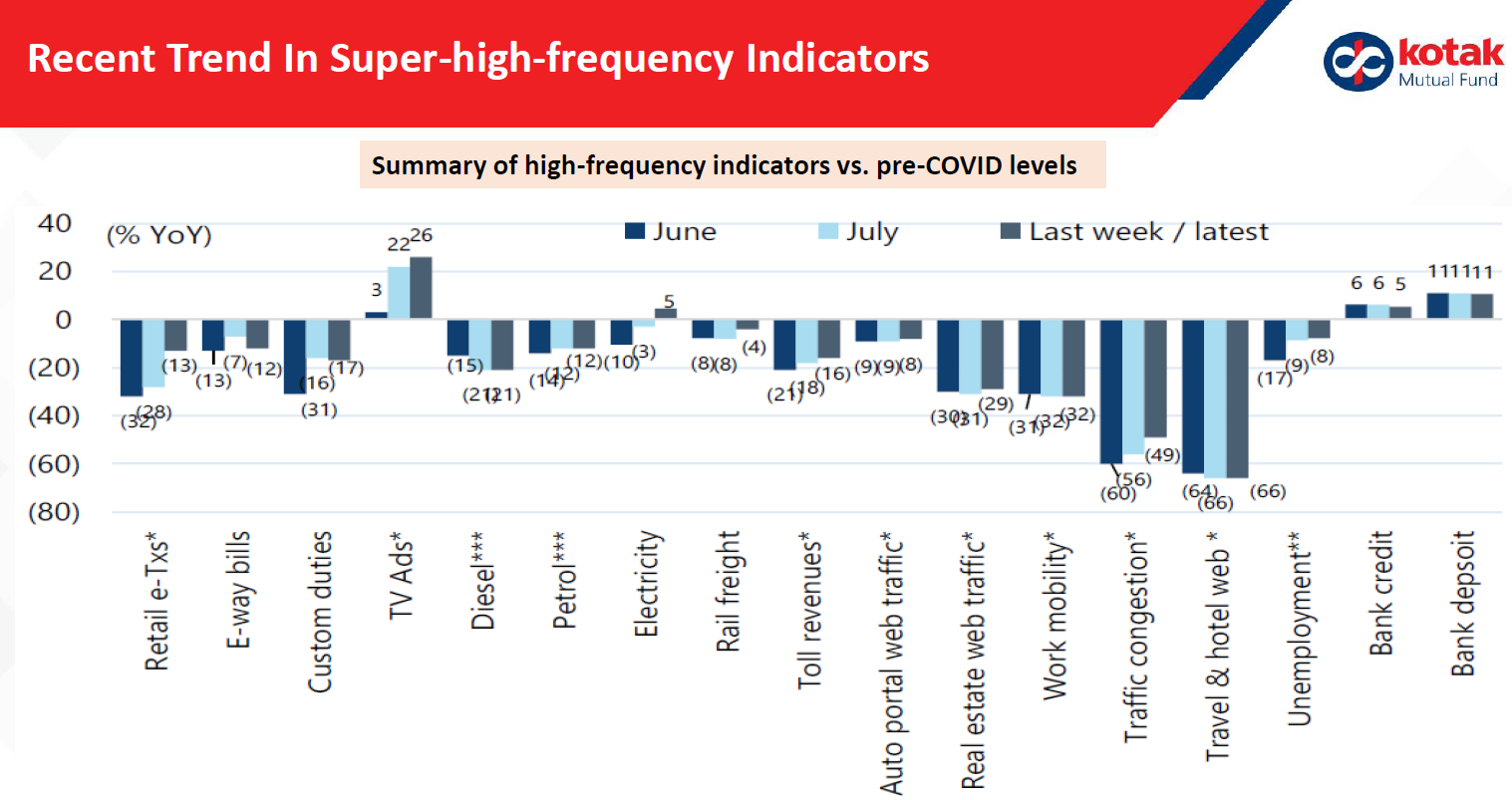

Some more high frequency data points which shows positive signs

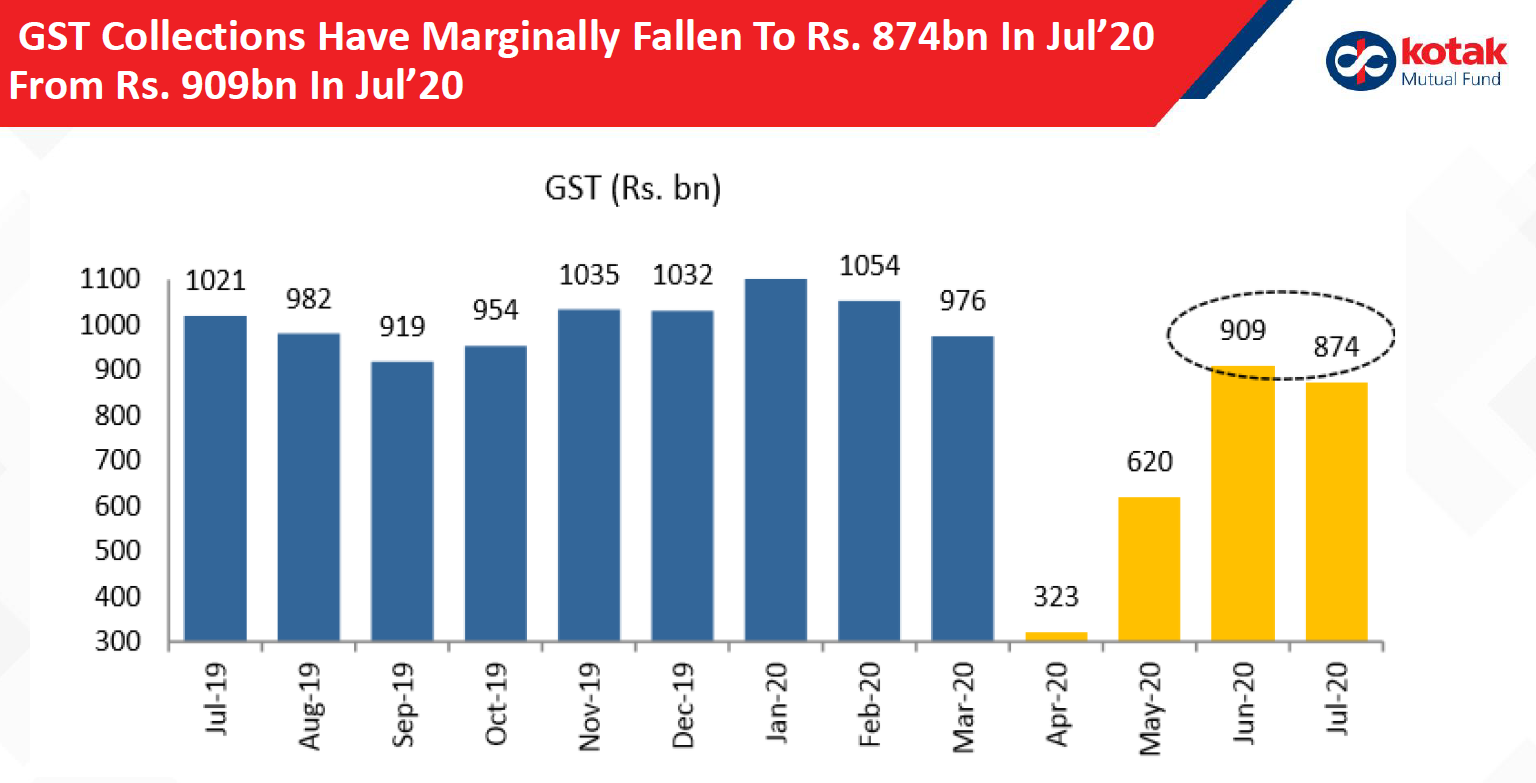

GST Collections have yet to come up to normal levels which is understandable owing to economy which is yet to fully recover

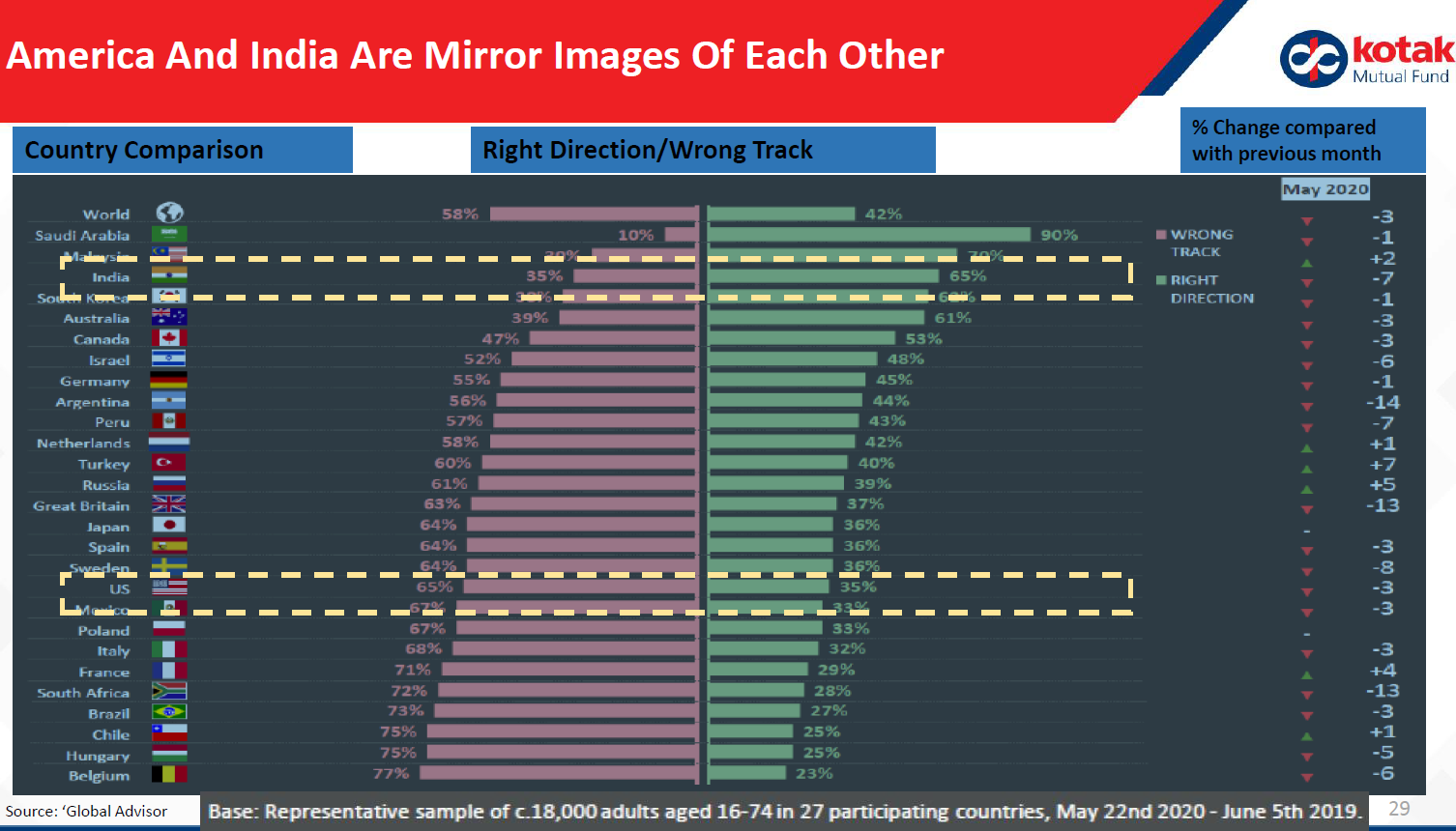

A question which comes to mind, are the Govt doing the right things. The data shows, that atleast in India it looks that we are progressing well – though opposite to what people think for US

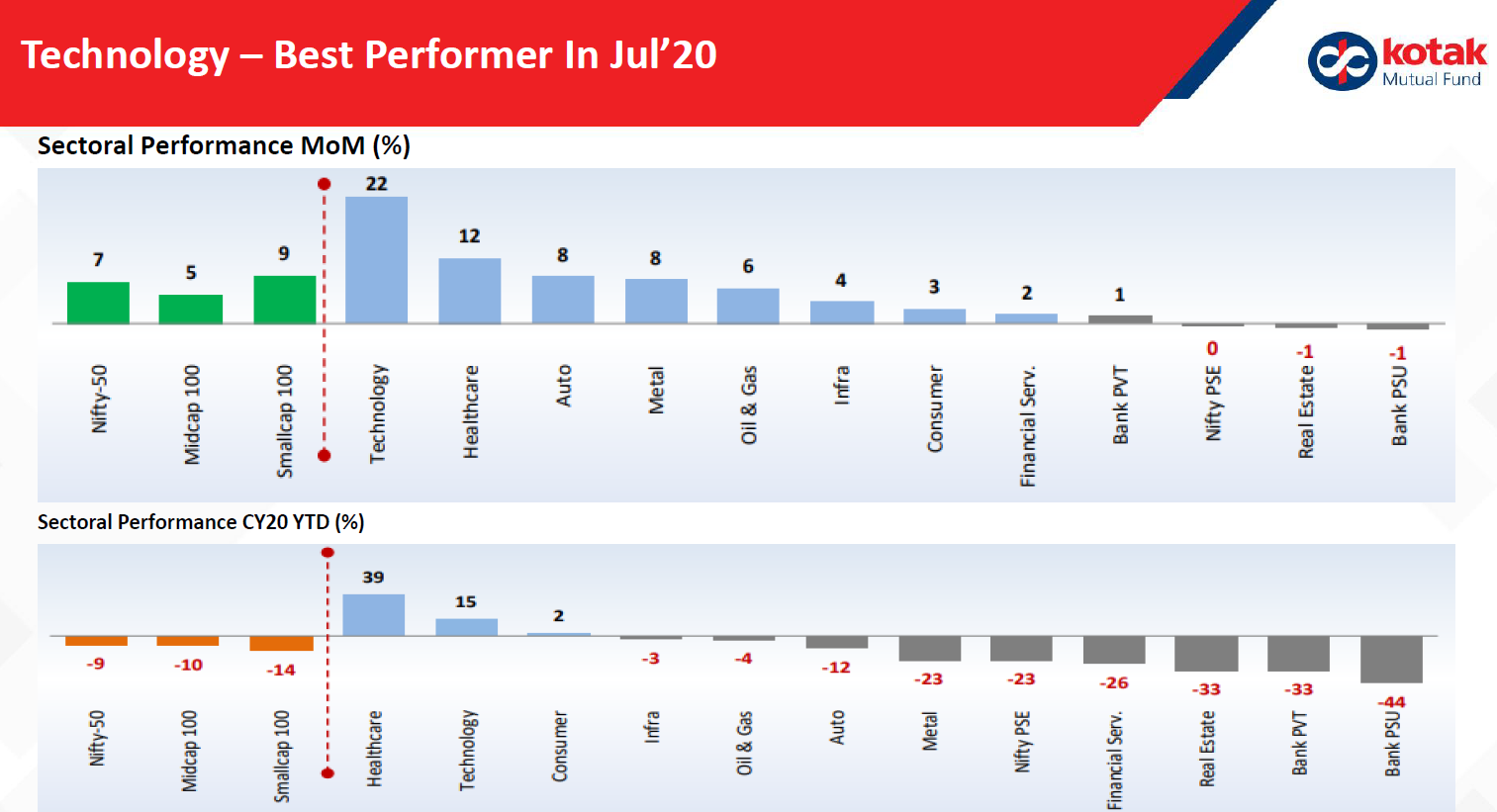

From the market performance till date, the drivers of this rally have been Healthcare & Technology. Banking is the laggard.

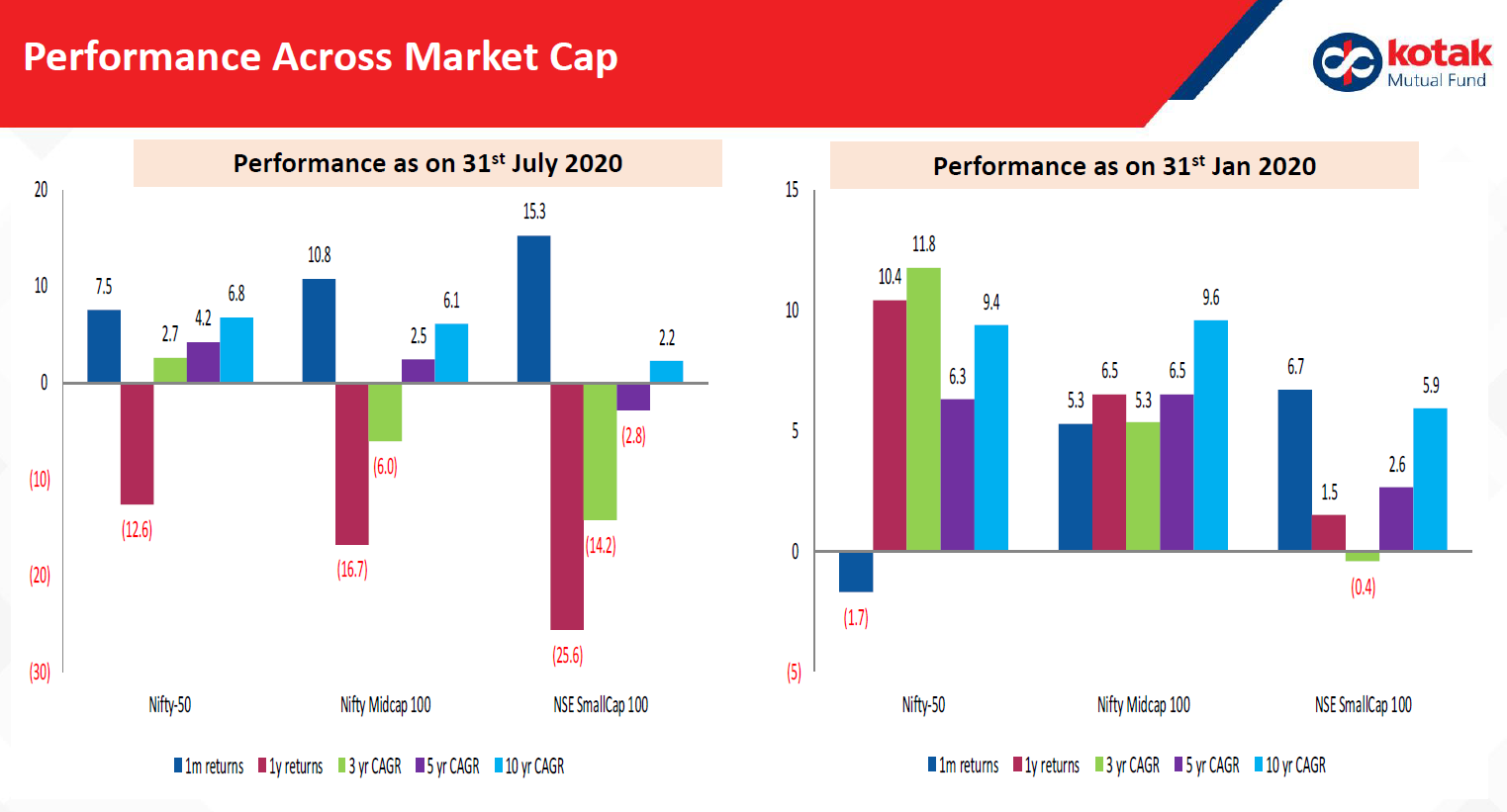

The current market correction has changed the return dynamics significantly. Right side shows returns as of Jan 2020 vs left as of July 2020 for short and long term returns.

Extreme amount of liquidity has been injected in the banking system.

Bond yields are also continuosly pushing lower and the gap between a good quality AAA and AA bond vs the Govt securities has come down drastically. One can already see that the yield on bond funds should be sub 5-6% from this point in future.

Gold – In times of uncertainity, it ends up being the asset class which is being chasen. The charts from 2007 onwards will show how volatile it can be.

Massive inflows in Gold are coming from ETFs. My personal view – Gold inflows via ETFs is extremely fickle. They come in quick and can go out even quicker. And with the size and scale of ETFs, this can mean a massive impact on either side. See the purple part in the column to see the growing scale

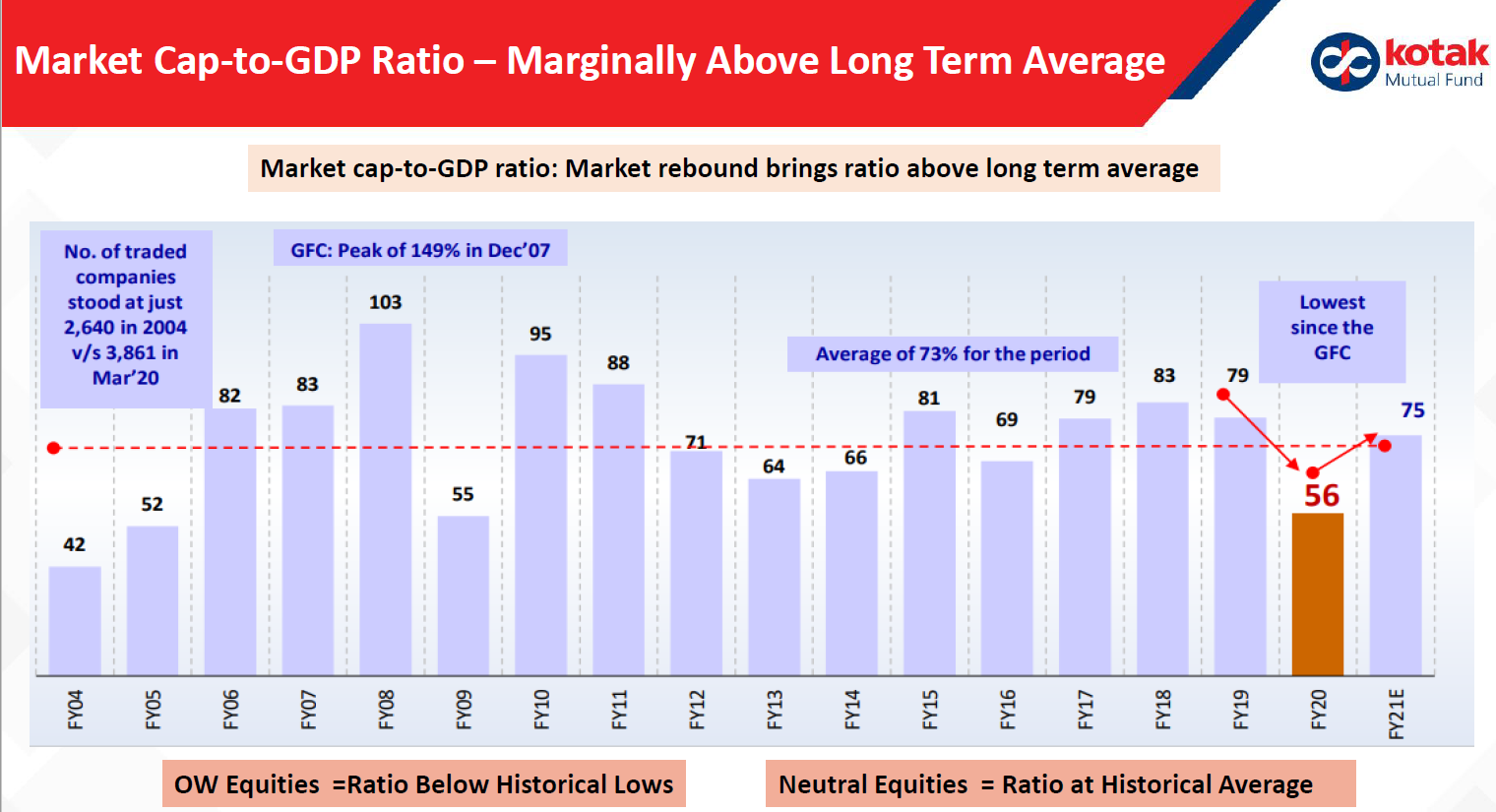

The valuations are now moderated now and one must not be overweight now.

Good view of various factors….though equity returns look good if invested during this period