If you are a salaried employee, it is likely that your employer would have provided you a mediclaim benefit, i.e. a group medical insurance policy to take care of any hospitalization expenses up to a specific amount. Depending upon an employer, this could be any where from Rs. 1 lacs to 5 lacs covering medical expenses for your family.

With rising medical costs, this amount is grossly insufficient. If one is hit by a critical illness, it would take the medical bills very quickly over a 10 lac rupees. An article published in Financial Express gave some estimates of the medical costs for a few major illness and it does not include incidental costs such as ICU charges :

Herceptin, one of the most effective drug for breast cancer, costs around Rs 75,000- Rs 1 lakh for a 440-milligram vial. Cancer patients need around 6 to 17 vials for reasonable treatment. You can quickly see the total rising up to around Rs. 17 lacs just for the drug cost.

Herceptin, one of the most effective drug for breast cancer, costs around Rs 75,000- Rs 1 lakh for a 440-milligram vial. Cancer patients need around 6 to 17 vials for reasonable treatment. You can quickly see the total rising up to around Rs. 17 lacs just for the drug cost.- One cycle of Avastin which is used for treating lung and breast cancer costs in excess of Rs 25,500, and each course requires between 5 and 10 cycles of injection.

- Glivec which is used in the treatment of multiple cancers, costs Rs 1.25 lakh for a month’s dose.

- Treating diseases of the cardiovascular system typically costs in excess of Rs 2-3 lakh in a city like Mumbai.

- An angioplasty can costs around Rs 1.5 lakh to Rs2.5 lakh,depending upon the type and number of stents being used, or where it is get done.

In summary, your existing medical insurance policy may be left helpless to fight against ever increasing medical bills and hence you should be geared to get your medical cover enhanced to cater to the unforeseen medical costs in future. This article will not go into the details of what a medical insurance policy is, as this is already covered in detail by our article Medical Insurance – Health is Wealth. With this article, we aim to highlight an innovative way to boost your current medical insurance coverage using a top-up insurance.

Top up Insurance

You may be familiar with the term insurance ‘excess’ or ‘deductables’ which is generally built into most of the insurance policies. Essentially it mentions the first ‘x’ amount which an insurance provider will not reimburse and hence would be borne by the policy holder. For example, if you have a medical insurance policy, it may mention about an excess of Rs. 5000. This means on your hospital bill of Rs. 50K, the insurance company will not pay you Rs. 5K and balance of Rs. 45K will be reimbursable.

Top up insurance works on the same principle and extends it further by providing a user an option to take a high voluntary excess (also called as deductable) of say Rs. 1 lac, 2 lac, 3 lacs and so on. The higher the voluntary deductable taken by the user, the cheaper will be the insurance policy. A person taking a top-up insurance policy is essentially taking an insurance to top up his / her existing insurance policy with a deductable equal to his existing insurance policy.

The Arithmetic

If you take a few quotes on Medical insurance policies, you will have notice that it is more expensive per lac to obtain a medical insurance policy for a lower denomination policy, e.g. upto Rs 1-2 lacs of cover. As the cover increases, the per lac cost decreases or at best remains constant. The logic behind this is – it is more likely for a person to have a medical bill of upto 1-2 lacs than a 10 lacs bill.

The positive side of this picture is, many of the employers would be providing a group medical insurance plan to their employees which covers immediate family of an employee (spouse and children. Parents are generally not covered). This is a very welcomed perk provided to employees as it covers basic medical costs for the entire family of an employee. In many cases, self employed people also have a basic medical insurance.

The pertinent question to ask is – what if the medical bills go beyond the existing medical insurance policy ? If you don’t have an insurance policy to cover you for this expense, the bills would have to be borne by you. Alternatively, you have an option to top up your existing medical insurance policy to cover for enhanced bills by using a top-up insurance policy.

How does Top-Up Feature Work

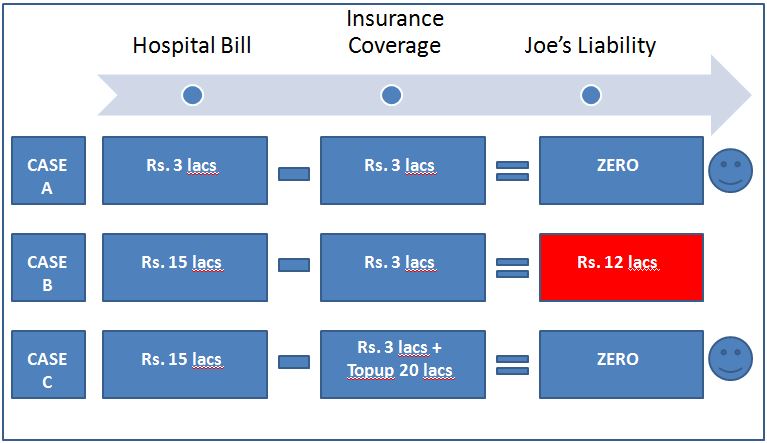

Lets take an example to make it easier to understand. Lets assume that Joe has an existing medical insurance policy which covers his family for upto Rs. 3 lacs of medical costs. Joe faces an unforeseen medical condition and is hospitalised. There are three scenarios which he could face financially where the medical expenses could be within his existing medical insurance policy or be much higher than his policy.

We would now be expanding more on Case C, where the top up insurance policy came to Joe’s rescue to shoulder extra medical bill beyond the initial Rs. 3 lacs medical bills. Joe had taken a top-Up insurance policy which would cover any medical expense beyond Rs. 3 lacs expense. Here, the first 3 lacs would be borne by any other mechanism other than by the topup insurance policy. Most likely, one would have an existing medical insurance policy to cover the initial amount of medical expense and balance to be borne by the top-up policy.

Key Features of Top-Up Insurance Policy

1. Deductable Amount

This is the most important feature of a top-up insurance policy. It will not cover upto the amount of deductable / excess mentioned in the policy. The higher the deductable, the cheaper the policy is. For example, if Joe’s medical insurance policy had a deductable of Rs. 5 lacs, upto Rs. 5 lacs the top up policy would not re-imburse. Beyond 5 lacs, the top up policy will cover upto the sum assured.

2. Not Linked to A Specific Policy

The best thing about a top-up policy is that it is not linked to any specific insurance policy or in that matter any insurance policy. All what it says, the first ‘x’ amount will not be borne by the top-up insurance policy. This amount of deduction can be borne by the policy holder or by any other insurance policy. Hence, a person has the flexibility to choose any insurance company for meeting the requirement for the basic few lacs of insurance requirements.

3. Protecting No-Claim Bonus

If you have an existing insurance policy, most of your ailments would be covered using its coverage without touching your top-up insurance policy. A positive effect is that your top-up insurance policy would be able to accumulate no-claim bonuses (if this is a part of your policy feature).

4. Initial 1-2 lacs deductable – Most Cost Effective

The first 1-2 lacs of deductables will make a disproportionate impact on reducing your insurance policy. The reason is simple – it is more likely for a person to make a claim on a medical insurance policy with no or low deductable. We would suggest having a deductable atleast equal to your existing medical insurance policy.

5. Deductable through the year vs per ailment.

This is a very important clause to look out for in your insurance policy. A perfect policy will consider all hospitalisation costs incurred within a policy year towards the initial deductable amount. A less desirable policy term would be where the deductable amount is per hospitalisation. For example, if Joe’s top-up insurance policy has a deduction of Rs. 5 lacs and he incurs hospitalisation bills of Rs. 1 lac in Jan, Rs. 4 lacs in June and Rs. 10 lacs in Nov, totaling to Rs. 15 lacs. The policy should consider the medical costs incurred throught the year towards initial deduction, i.e. 1 lac in Jan and 4 lacs in June are allowed to be considered and Rs. 10 lacs are entirely borne by the top up policy as Rs. 5 lacs expenses in the year have already been borne by the policy holder / other insurance policy. In a less desirable policy, Rs. 1 and 4 lacs bill will not be paid as they are less than 5 lacs. It will also not pay Rs. 10 lacs bill in full as it will deduct Rs. 5 lacs deductable from the individual bill.

6. Tax Rebate – 80D

This should not be the driving factor behind your decision to take a top-up medical insurance plan, but is just a cherry on the top of the cake. Current tax year comes with enhanced exemption towards medical insurance for individuals under section 80D :

- Individuals – upto Rs. 25,000

- Medical insurance for parents – additional Rs. 30,000

This benefit tends to be under utilised as most of the people do not end up taking medical insurance after having the basic insurance being provided by their employers. If you take top-up insurance, you can avail tax rebate on the insurance premium based upon your tax slab. So if you are a 30% tax payer, you can avail 30% tax rebate on the insurance premium paid by you.

We hope you would be able to get an understanding of this interesting financial product which allows you to enhance your medical insurance coverage with minimal drain on your purse. For further assistance, please contact your financial advisor.