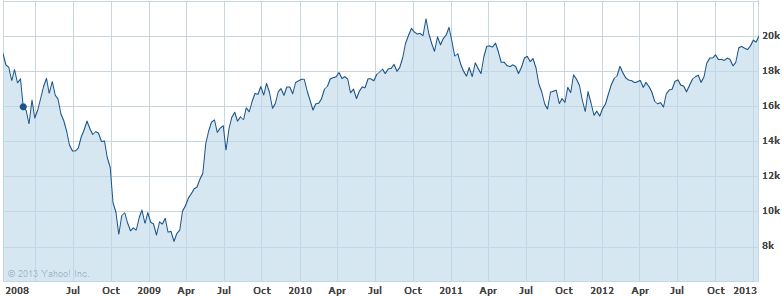

Not sure if you have seen the movie Saas Bahu and Sensex, one of the most crazy and funny movies made around the story where stock markets make people rich. It was amazing to see CNBC’s famous editor Udyan Mukherjee dancing to the tune of Sensex’s jolly ride and touching its life time high. The situation is quite similar now. Have a look at the chart below which shows the dance steps BSE Sensex did since 2008 :

* Sourced from Yahoo finance

The rationale behind just looking from 2008 and not longer is owing to the fact that many of us as investors have entered into the interesting and volatile world fo investing only since then and are facing a dilemma today of whether we should continue to invest beyond 2013 or atleast encash our profits.

So, the Sensex has just touched 20K levels in January 2013 bring some smiles to a lot of investors who are now starting to see some green ticks on their investment portfolios which they have been holding very patiently as well as frustratingly long for past couple of years. These portfolios have seen the test of time and have gone through blood bath in the roller coaster ride which the stock markets took from 2008 till the end of 2012. I can not forget the yo-yo where the stock markets were at 19K mark in 2008 and took a massive beating till March 2009 where they dropped till 9K levels in just 1 year. Then came a steep climb from 9K to around 17K in just next 6 months. After that came a painful period of 1 year where the markets just kept loitering in a range for a year and then took a steep jump to 21K by Nov 2010. Many gullible investors started to invest believing in India’s growth story and after that there was a seemingly never ending down turn till the third Quarter of 2012 where the markets again started to inch up and have finally reached back at 20K levels. What in store for future ? Perhaps no one knows. If you can look back in the past, all the so called experts who were predicting the future of markets were in most cases proved wrong. They kept on changing their predictions on a regular basis to suit the moods of the markets. Would I trust on their prediction now – Probably NOT !!

You might be wondering why I am trying to blabber upon Stock market’s volatility which is so commonly known. Well I am trying to console the hearts and souls of those patient investors who have been trying to make some returns (if not massive killings) out of their meagre savings. These testing times have uprooted the financial foundations of so many families who couldn’t either have patience or tried to speculate upon the movements of the markets. Hence, through this article, I am trying to arrive at the next steps which such investors may take with their investments.

Whats next ?

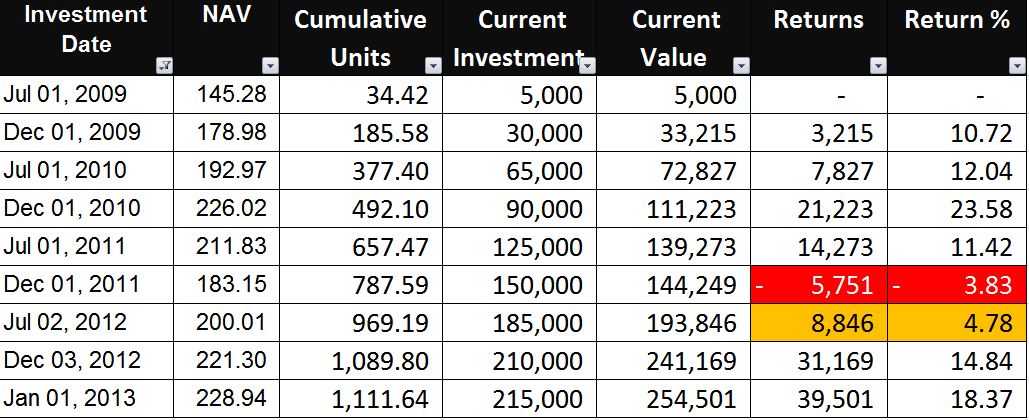

If you have been investing via SIPs in a mutual fund since 2009, what would you be sitting upon ? Let me take a hypothetical case of an investor who has been investing Rs. 5,000 per month in one of the top performing funds – HDFC Top 200 since 1 July 2009. I am purposefully excluding the extraordinary period from Jan 2008 to June 2009. A summary of what he would have gone through in past 3.5 years is in the table below. The fourth column reflects his current investment amount (cost) and fifth column is showing the market value of his investments on the specific day in row. It is quite obvious that there is a lot of volatility in the returns and in 2011, the returns even turn negative (in red)! Where I have highlighted the cells in Orange, it shows a sub-standard return of less than 5%.

In a graphical sense, I have tried to show how volatile is the market value of the investment over a period of about 4 years. The red line shows the market value and blue is the cost of investments (increasing by 5K per month). It is evident that several times in 4 years the market value went below the cost (meaning losses) !

If you put yourself in the boots of an investor who has never invested into Equity markets and has always been a fan of fixed income based products like FDs, RDs, PPF, etc., this is a night mare kind of a situation. Such an investor’s expectations from his investments is good stable returns, even though it is capped to maximum 8-10%. Investments and losses are mutually exclusive terms for this person and ups and downs of the market value (with red losses) would possibly pep up his heart beats. So even though he may be sitting at a handsome returns of 18% plus, the stress which this investor would have gone through (owing to his expectation of a stable return) can not compensate this return versus a 10% return of a FD. If you were such a person, what would be the first thing which would come in your mind. Your answers may be any one from the below :

(A) Sell the bloody investment and exit from it. It is not worth the stress. I am happy with my stable return of 10% from FD.

(B) Let me sell part of my investments and make some profits. Atleast I have encashed some returns in case the markets go down again.

(C) Sell all investments and I shall invest when markets come down. I can’t trust the markets currently.

(D) I will continue to invest for a long term horizon and will not sell currently. Stock markets are volatile and in long run, things will be much better.

What is my recommendation

I am a firm believer of investing in Equity markets – whether directly or via mutual funds. Equities are volatile instruments and can no where give an investor the mental comfort of a stable returns as in case of a fixed deposit. However, in the longer term, their returns would definitely surpass Fixed Deposits. I believe, atleast 1.5 – 2 times of the prevailing rate for FDs, otherwise why would corporates want to do their businesses when they can get the similar returns by investing into FDs.

Consider this – in case of a 5-10 year FD, do you go now and then to the bank and get your FDs liquidated to book some of the interest income as cash ? If not, why do you consider your long term Equity investments differently ? Fair enough – in case of FD you know the maturity amount initially and this is not the case in Equities. But that is the reason why Equities are classified as a risky product for a long term investment tenure only.

All of your investments into Equities should be over 5-10 years investment horizon. If your financial advisor told you to invest into Equity markets for 1-3 years investment horizon, I would strongly recommend you to go out shopping for another sound minded advisor. And once you have made your decision to enter into such an instrument, keep your nerves calm and avoid the temptation of either selling the investments to book profits or exiting in haste to avoid further losses.

If you want to liquidate all your holdings to invest in better times when markets would be lower – I would wish you good luck. My experience with my clients has been quite the contrary. When it is a good time to invest (when markets are low), the amount of bad news and negativity in the markets scares the most sound and brave hearted investors. Every one keeps on waiting for SOME MORE TIME. And that time never comes. Just ask this question to yourself – why didn’t you invest in the great falls of 2009 ?

Timing the markets

Then all of a sudden the markets take a U turn and the investors who have been waiting to invest keep on waiting for eternity. At this moment, they face another dilemma. An item (essentially an investment) which they could earlier buy at Rs. 100 a couple of weeks back when the markets were low, would now be available at Rs. 115 or more. Since they have seen the rate of Rs. 100 just some time back, Rs. 115 looks expensive (even though it may still be a cheap price). They would then want to wait a bit longer so that when the prices come back to Rs. 100, they can invest. But now, Rs. 115 climbs up to Rs. 120, 125 and higher… and these investors are sitting with their pile of cash earning them meagre or no return. Frustratingly enter into the markets when the investment is quoting at Rs. 150. But by this time, the investment has become so expensive that its value starts crashing back to Rs. 130. The poor investor is now scared of further devaluation of his investment (dropping from Rs. 150 to Rs. 130). His fear factor forces him to sell his investment and book a loss of Rs. 20 in order to prevent further losses. The markets drop a little further to Rs. 125 bringing some cheer to the investor and making him pat on his back considering he took an intelligent decision to sell his investments at Rs. 130. And guess what, the markets zoom up to Rs. 135 and poor investor is again gazing in the black hole cursing every thing possible in financial markets except his wrong doings of trying to time the markets. Hence, my advise would be to stop timing your purchase and keep on investing in a systematic manner via your SIPs.

I should atleast book some Profits

If you want to sell some part of your investments and book profits – my query is – what would you do with such profits ? What if the markets went a bit higher and you lost an opportunity to make further returns. Your equally right counter argument can be – what if the markets went lower and you lost the opportunity to encash the returns. Fair enough, however, if you look into the chart above, you would notice that for a long term investor, these opportunities will keep on coming every now and then. If you try to knock your investments out by encashing your profits, you would severely impair your investment’s capacity to generate further returns in future. Such profits will then sit in your bank account waiting to be invested and would probably end up getting used towards household expenses. Perhaps the question to ask yourself is – do you really need to encash your investments to fund any emergency or expenses? If you are earning your regular income (via business or salary), the answer in most cases would be a No.

By encashing, you would also expose yourself to certain costs such as an exit load of around 1% and short term capital gain tax for investments done within 1 year. And the advantage, in my views is not material !

Hence in my opinion – PLEASE leave your investments alone and continue to fund them on a regular basis. Better times are yet to come and in 5-10 years down the line you would be sitting on an amazing retirement pot overflowing with returns. But that is only possible if you continue to invest and avoid the temptation of encashing your returns every now and then. If all what I have mentioned comes to you as a surprise then you clearly need a good financial advisor. Agents and distributors do not at times do a good job in educating investors on the products they are trying to sell in order to earn their commissions. Perhaps, at times they are also not sufficiently educated to know about such details – better option – get a dosage of learning and I am sure after that you would be better prepared to handle the markets.

I completely agree with the argument of investing in equities with a long time horizon and the concept of systematic investing. However, the returns shown for the example of HDFC Top 200 Fund are misleading as they are XIRR returns and not absolute or annualised. The manner of showing SIP returns should be to calculate annualised returns for every installment and then average the same. The results will be vastly different.

Instead of taking a single asset class approach, one should look at multi asset investing which does not compromise returns but reduces the volatility in the portfolio

I think the suggestion here is not to exit or book profits unless money is required for expenses in the near future, or a better alternative investment opportunity has been identified. But at the same time, investments are means to an end and not ends in themselves,and I believe a target return percentage should be set beyond which profits should be booked either by cashing out or re-allocating funds as per the target asset allocation plan. Views?

You have a very valid point – I should have taken XIRR as a more valid way to reflecting returns. However, this is just a simple example to put my point across.

Avoiding diversification across diff asset classes is like giving invitation to volatility. Good points Funny Guy.

AB – I like your comment and specifically that investments are means to an end. However, that end needs to be agreed at the start – which should be a financial goal (e.g.retirement) and not a trading goal (achieving a % return). A target % return will promote early encashment which may not help in fulfilling your end financial goals.